Industrial Water Treatment Chemicals Market Snapshot: Market Size, CAGR, and Growth Outlook to 2032

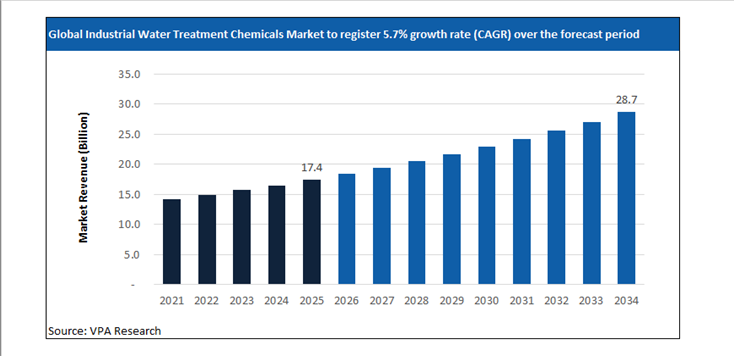

Global Industrial Water Treatment Chemicals Market Size is projected to hit $28.7 Billion in 2034 at a CAGR of 5.7% from $17.4 Billion Million in 2025.

The report analyzes the global Industrial Water Treatment Chemicals Market across diverse segments including By Product Type (Scale Inhibitors, Corrosion Inhibitors, Coagulants & Flocculants, Biocides & Disinfectants, pH Conditioners & Softeners, Antifoaming Agents & Defoamers, Oxygen Scavengers & Sludge Conditioners), By Application (Cooling & Boilers, Effluent Water Treatment, Raw Water Treatment, Water Desalination), By End-Use Industry (Food & Beverage, Power Generation, Oil & Gas, Pharmaceuticals & Microelectronics, Pulp & Paper and Mining).

The Industrial Water Treatment Chemicals Market Market at a Glance (2026)

Process Water Integrity, Chemistry Precision, and Regulatory-Critical Demand

The industrial water treatment chemicals market is structurally defined by process water integrity and chemistry precision rather than discretionary environmental spending. Industrial water treatment chemicals are indispensable inputs used to control scaling, corrosion, fouling, microbiological growth, and contaminants across power generation, oil and gas, chemicals, metals, food processing, pulp and paper, mining, and pharmaceuticals. Performance is governed by molecular formulation, dosage accuracy, compatibility with water chemistry, and stability under fluctuating operating conditions. Procurement decisions prioritize verified treatment outcomes, regulatory compliance, and operational continuity because water-related failures directly cause equipment damage, production downtime, and regulatory penalties.

In 2025, Ecolab expanded industrial water treatment programs focused on cooling water and boiler optimization for energy-intensive manufacturing sites. During the same year, Veolia advanced industrial water chemistry solutions aligned with zero-liquid-discharge and reuse objectives in Asia and the Middle East. These developments underscore how the global industrial water treatment chemicals industry is anchored in mandatory process control rather than voluntary sustainability initiatives.

Power Generation, Manufacturing, and Sector-Specific Utilization

Power generation remains one of the most structurally significant demand anchors for the industrial water treatment chemicals market. Thermal power plants, combined-cycle facilities, and industrial cogeneration systems depend on boiler and cooling water treatment to prevent scaling, corrosion, and efficiency loss. Even marginal degradation in water chemistry can reduce heat transfer efficiency and increase fuel consumption, making chemical programs core to plant economics. In 2025, utilities and industrial power operators across Asia-Pacific continued to optimize water treatment regimes to reduce water intensity and comply with tightening discharge standards.

Manufacturing and processing industries represent another critical demand segment. Chemical plants, refineries, steel mills, and food processing facilities generate complex wastewater streams requiring tailored coagulation, flocculation, pH control, and biocide programs. Water reuse initiatives further increase reliance on advanced chemical treatment to maintain consistent process water quality. Europe and North America emphasize compliance and documentation, while emerging markets prioritize operational reliability and reduced freshwater intake due to resource constraints.

Environmental Regulation, Digital Water Management, and Competitive Dynamics

Environmental regulation is the dominant structural driver shaping the industrial water treatment chemicals market. Discharge limits, water abstraction controls, and hazardous substance regulations force industrial operators to maintain consistent treatment performance. In 2025, European Chemicals Agency continued oversight of water treatment substances under chemical safety frameworks, reinforcing the need for compliant formulations and transparent reporting. Similar enforcement actions by regional regulators in Asia and North America sustained demand for proven treatment chemistries.

Global Industrial Water Treatment Chemicals Market Market Dynamics: Growth Drivers, Restraints, and Opportunities

Strategic Market Drivers: What’s Fueling Growth in 2026?

The Industrial Water Treatment Chemicals Market market report provides a comprehensive assessment of the structural and technical factors shaping the market’s evolution in 2026 and beyond. It evaluates demand-side shifts, supply-side constraints, regulatory influences, and technology-led disruption impacting both established players and new market entrants. The Industrial Water Treatment Chemicals Market market analysis details the impact of changing end-use requirements, evolving customer specifications, and increasing performance expectations across countries. Further, key drivers and opportunities are mapped across regional and application-level dynamics.

Profit Prioritization and Portfolio Rebalancing

-

Asset Rationalization: Tier 1 players are aggressively divesting low-margin, commoditized assets to reallocate capital toward high-purity, differentiated offerings with superior pricing power.

-

Operating Leverage: Amidst persistent raw material volatility, companies are leveraging Digital Twins and AI-driven manufacturing to optimize OpEx.

-

Specialty Transition: Strategic investments are now concentrated in high-growth niches where customized formulations and technical barriers to entry protect EBITDA margins from global overcapacity in basic chemicals.

A Deep Dive into Emerging Market Hubs

Rapid economic growth, coupled with demand for Industrial Water Treatment Chemicals Market are driving the investment focus on these markets. In particular, India, China, Southeast Asia, Brazil, Eastern Europe, and Latin American markets are registering higher than the global average growth rate. The urban population is expected to reach 6 billion by 2045, around 1.3 times the surge from 2023 levels. Rapid industrialization, infrastructure development, urbanization, and expanding domestic consumption are driving above-average demand growth across markets. Leading Industrial Water Treatment Chemicals Market companies are accelerating investments in local manufacturing, regional supply chains, and application-specific product development to capture these opportunities.

Emerging Opportunities: Untapped High-Growth Niches in the Post-Pandemic Recovery

The post-pandemic landscape for the chemical industry shifted from crisis management to strategic opportunity. In 2026, leading companies are focused on supply chain regionalization, the hygiene-sustainability nexus, and the digital leap in R&D. The Industrial Water Treatment Chemicals Market market is witnessing the emergence of niche, high-growth segments driven by evolving customer needs and regulatory drive. Demand for customized formulations, performance-enhancing solutions, and application-specific variants is rising across advanced manufacturing, specialty end-use industries, and sustainability-led applications. The report identifies underpenetrated segments where innovation, technical differentiation, and faster go-to-market strategies can unlock disproportionate value.

Industrial Water Treatment Chemicals Market Market Challenge- Impact of Geopolitical Uncertainty on Market Stability

In 2026, geopolitical risk has become a structural variable shaping the Industrial Water Treatment Chemicals Market market rather than a short-term disruption factor. Ongoing trade realignments between the U.S., China, and the EU, coupled with sanctions regimes, export controls, and industrial policy interventions, are directly influencing sourcing strategies, production footprints, and pricing stability across the Industrial Water Treatment Chemicals Market value chain. Regional disparities in energy pricing, port congestion risks, and shipping route instability are creating uneven cost structures among global Industrial Water Treatment Chemicals Market producers. Accordingly, Industrial Water Treatment Chemicals Market companies with regionally diversified production assets and localized supplier ecosystems are demonstrating higher margin stability compared to export-reliant peers.

Industrial Water Treatment Chemicals Market Market Strategic Assessment: SWOT, Five Forces, and Value Chain Analysis

Scenario analysis

Amidst varying regulations, trade patterns, supply chain dynamics, and market dynamics, the scenario analysis allows firms to stress-test their current business models. The chapter provides three distinct ‘What-If’ pathways for the Industrial Water Treatment Chemicals Market market through 2032- high growth, low growth, and reference cases. The detailed forward-looking assessment ensures that strategic decisions made today remain viable across a range of potential economic and regulatory outcomes.

Value Chain Analysis

The report identifies key players across the Industrial Water Treatment Chemicals Market industry value chain, tracing the flow from procurement to end-user. By understanding supplier dependencies, processing intensity, distribution dynamics, and customer power at each stage, stakeholders can identify opportunities for vertical integration, strategic partnerships, localization, or operational optimization.

Porter’s Five Forces Analysis

The Porter’s Five Forces analysis chapter incorporates quantitative scoring and weighted impact evaluation for each competitive force within the Industrial Water Treatment Chemicals Market market. This section helps objectively measure industry attractiveness, margin sustainability, and competitive risk using a standardized analytical framework. Companies can evaluate the bargaining power of suppliers and buyers, the threat of substitutes and new entrants, and the degree of rivalry among existing players.

Market Segmentation: Historical and Projected Market Revenue Forecast

Revenue Growth Strategies for Industrial Water Treatment Chemicals Market Segments

The report provides the Industrial Water Treatment Chemicals Market market size across By Product Type (Scale Inhibitors, Corrosion Inhibitors, Coagulants & Flocculants, Biocides & Disinfectants, pH Conditioners & Softeners, Antifoaming Agents & Defoamers, Oxygen Scavengers & Sludge Conditioners), By Application (Cooling & Boilers, Effluent Water Treatment, Raw Water Treatment, Water Desalination), By End-Use Industry (Food & Beverage, Power Generation, Oil & Gas, Pharmaceuticals & Microelectronics, Pulp & Paper and Mining). Market size outlook across the segments is provided at the global, North America, Europe, Asia Pacific, South and Central America, and the Middle East and African regions. Across each segment, the report analyzes the growth prospects, post-pandemic recovery, and country-specific dynamics.

Regional Outlook for Industrial Water Treatment Chemicals Market Manufacturers

United States Industrial Water Treatment Chemicals Market Market Size and Share Analysis- Evolving Trade Policies and Supply Chain Reshuffling

The United States Industrial Water Treatment Chemicals Market market is being reshaped by evolving trade policies, industrial localization initiatives, and a reconfiguration of global supply chains. The outlook for 2026 is moderately higher relative to 2025, driven by policy-driven sourcing decisions, domestic manufacturing incentives, and strategic supplier realignment.

Global GDP forecasts fell to 3.0% in 2025 and 3.1% in 2026, with US growth slowing to 1.8% and 1.4%, respectively. Tariffs on critical intermediates have added around 0.5 percentage points to core inflation, squeezing the margins of downstream manufacturers. Similarly, an estimated 20% of manufacturers are likely to deploy physical AI to mitigate labor shortages in the US. Over the forecast period, as domestic pricing, margin profiles, and capacity utilization increasingly correlate with U.S.-specific trade exposure, logistics costs, and policy alignment, companies focus significantly on supply-chain optimization.

Canada Industrial Water Treatment Chemicals Market Industry Forecast 2026–2032- Increasing role in North America Supply Chain realignment

Canada’s real GDP growth is projected to average 1.25% to 1.5% in 2026, a modest recovery from the 1.3% growth seen in 2025. Unlike the high-volume commodity focus of previous decades, the current market is driven by high-value specialty segments. Strong end-user demand from Ontario, Alberta, Quebec, British Columbia, and other provinces is shaping the long-term growth strategies. The report analyzes the key market drivers and provides the Canada Industrial Water Treatment Chemicals Market market size outlook over the forecast period to 2032.

Mexico Industrial Water Treatment Chemicals Market - Companies are investing in Nearshoring hubs

Nearshoring into Mexico and Canada is accelerating, with the US-Mexico trade projected to grow by $315 Billion by the end of the decade. The American Chemistry Council (ACC), the National Association of the Chemical Industry of Mexico (ANIQ), and the Chemistry Industry Association of Canada (CIAC) are focusing on renewal and strengthening the USMCA. Geographic proximity to the United States enables just-in-time supply models, making Mexico a strategic production location for downstream chemical derivatives, resin conversion, coatings, adhesives, and formulation-based specialty products.

Germany Continues to Dominate the European Industrial Water Treatment Chemicals Market Industry

German giants are divesting non-core assets and emphasizing specialized applications, technical precision, and high-value customer solutions. For instance, Henkel’s $2.5 billion acquisition of Stahl Holdings in February 2026. Leading Industrial Water Treatment Chemicals Market companies are formulating strategies to mitigate short-term effects, including supply chain disruptions and destocking, and longer-term structural dynamics. Over the long-term future, demand outlook remains steady across key value chains, driving investments in new product launches and widening distribution channels.

UK- Post-Brexit Divergence and Specialized Clusters

The United Kingdom chemical industry in 2026 is shaped by divergent structural forces combining cost pressure with specialization-driven resilience. European natural gas prices remain structurally around 3.5× higher than U.S. levels, constraining energy-intensive bulk chemical economics and accelerating a pivot toward higher-value specialty chemicals, performance materials, and formulation-led production. Industry restructuring across the region is evident, with chemical plant closures in Europe increasing sixfold since 2022, according to Cefic, reinforcing the UK sector’s move away from commodity exposure toward efficiency-focused, technology-enabled operations. At the same time, logistics capacity is expanding, with the UK chemical logistics market growing at roughly 5% annually to reach about $8 billion in 2026, strengthening the country’s role as a storage, distribution, and re-export hub for specialty and regulated chemical flows.

China and India account for over 40% of global demand

China’s Industrial Water Treatment Chemicals Market industry is witnessing rapid capacity expansion, technology-led upgrading, and demand reorientation, with accelerated investment across value chain segments reshaping competitive dynamics. The $1.5 trillion chemical industry remains a primary engine of GDP growth, with a government-mandated target of 5% average annual growth in industrial added value through year-end 2026.

Demand fundamentals are also shifting structurally: by 2030, China and India together are projected to account for 40% of global middle-class consumption, up from less than 10% in 2010, indicating long-term expansion in consumption-driven Industrial Water Treatment Chemicals Market applications. Among end-user markets, Guangdong, Jiangsu, Shandong, Zhejiang, Sichuan, and others are widely focused on by vendors.

India remains a significant outlier with a projected 6.6% GDP growth in 2026, driving a surge in Industrial Water Treatment Chemicals Market demand. The government's $1.4 trillion National Infrastructure Pipeline is a massive driver for the market outlook. The Indian government is expected to expand the Production Linked Incentive (PLI) scheme for specialty chemicals in 2026.

Japan: Maintaining Dominance in High-Performance Segments

Japan’s Industrial Water Treatment Chemicals Market industry in 2026 is concentrated in high-performance, specification-critical segments where technical qualification barriers protect margins. Japan’s chemical sector remains one of the world’s most innovation-dense. In 2026, R&D spending in the sector continues to exceed $2.1 Billion annually, with Tokyo and the Kanto region serving as the global hubs for research. Persistent public-sector funding worth ¥4 trillion has moved capital toward advanced materials. To sustain competitive positioning in the evolving environment, Japanese firms can unlock growth by developing new markets through business model transformation and differentiated customer engagement strategies, reflecting the industry’s shift beyond product-led competition toward solution-oriented value creation.

Southeast Asia: The New Manufacturing Core

Southeast Asia is emerging as a primary manufacturing and chemical production growth zone, supported by industrial policy, infrastructure expansion, and supply chain diversification. Vietnam is advancing sector expansion under its Chemical Industry Development Strategy 2030, targeting average annual industry growth of 10–11% through 2030, with emphasis on petrochemicals, downstream plastics, industrial chemicals, and specialty materials serving electronics, construction, and export manufacturing.

The regional economy continues to be resilient, adapting to the shifting landscape and with momentum varying across countries and sectors. Concurrently, Indonesia is accelerating industrial capacity through its National Medium-Term Development Plan (RPJMN), which includes $414 billion in infrastructure investment, strengthening ports, energy systems, and industrial corridors critical for chemical logistics and processing industries.

Middle East- Rapid Economic Growth Supports Potential Business Expansion Opportunities

The Middle East chemical industry is strengthening its position as a global production and export hub through sustained capital deployment, feedstock integration, and downstream diversification. Between 2023 and the end of 2026, the region is tracking around 160 capital projects valued at more than $55 billion, reflecting continued investment in petrochemicals, polymers, specialty derivatives, and industrial chemicals.

The regulatory environment has become increasingly fragmented across geographies. Abundant hydrocarbon feedstocks, integrated refinery-petrochemical complexes, and export-oriented infrastructure provide structural cost advantages that support both commodity and higher-value chemical chains. In Saudi Arabia, the National Industry Strategy targets a fourfold increase in downstream chemical output by 2035, signaling a shift from base petrochemical exports toward specialty materials, performance polymers, and conversion industries.

Competitive Analysis- Intensity of Competition and Market Share

Companies are increasing R&D expenditures by 2-3% while high-intensity segments are witnessing an 8-9% increase in expenditure. The global Industrial Water Treatment Chemicals Market industry is characterized by intense competition with companies focusing on profit margins through widening end-user applications. Leading companies, including Ecolab Inc. (Nalco Water), Veolia Environnement S.A., BASF SE, Solenis LLC, Kurita Water Industries Ltd., Kemira Oyj, Suez S.A., Dow Inc., Nouryon, SNF Group, are analyzed in the study. For each company, a detailed business description, SWOT profile, and products and services benchmarking are provided.

Industrial Water Treatment Chemicals Market Market Segmentation

By Product Type

Scale Inhibitors

Corrosion Inhibitors

Coagulants & Flocculants

Biocides & Disinfectants

pH Conditioners & Softeners

Antifoaming Agents & Defoamers

Oxygen Scavengers & Sludge Conditioners

By Application

Cooling & Boilers

Effluent Water Treatment

Raw Water Treatment

Water Desalination

By End-Use Industry

Food & Beverage

Power Generation

Oil & Gas

Pharmaceuticals & Microelectronics

Pulp & Paper and Mining

Top companies in the Industrial Water Treatment Chemicals Market industry

Ecolab Inc. (Nalco Water)

Veolia Environnement S.A.

BASF SE

Solenis LLC

Kurita Water Industries Ltd.

Kemira Oyj

Suez S.A.

Dow Inc.

Nouryon

SNF Group

Countries Included-

-

North America- US, Canada, Mexico

-

Europe- Germany, France, UK, Spain, Italy, Nordics, Others

-

Asia Pacific- China, India, Japan, South Korea, Australia, Southeast Asia, Others

-

Latin America- Brazil, Argentina, Others

-

Middle East and Africa- Saudi Arabia, UAE, Other Middle East, South Africa, Other Africa

Latest Market Updates In Chemicals

Support this report with fresh, same-industry updates that strengthen topical depth and internal linking.

By Application

Raw Water Treatment

-Deoiling Polyelectrolytes (DOPE)

-Organic Coagulants

-Flocculants

-Filtration Aids

-Dewatering Aids

-Others

Water Desalination

-Biocides

-Cleaning Agents

-Antiscalants

-Flocculants

-Defoaming Agents

-Others

Cooling & Boilers

-Sludge Controllers

-Antifoams

-Antiscalants

-Oxygen Scavengers

-Others

Effluent Water Treatment

-Deoiling Polyelectrolytes (DOPE)

-Organic Coagulants

-Flocculants

-Filtration Aids

-Dewatering Aids

-Others

Others