Computed Radiography and Digital Radiography Market Snapshot: Market Size, CAGR, and Growth Outlook (2021 to 2034)

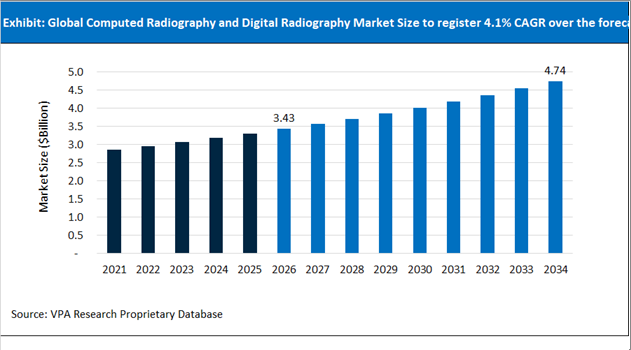

The global Computed Radiography and Digital Radiography Market size is forecast to increase from $3.43 Billion in 2026 to $4.73 Billion in 2034 at a CAGR of 4.1% between 2026 and 2034.

The Computed Radiography and Digital Radiography market report provides detailed analysis and outlook of Computed Radiography and Digital Radiography segments including By Technology: (Computed Radiography, Direct Digital Radiography ), By Portability: (Fixed Systems, Portable Systems), By Type: (Static Imaging, Dynamic Imaging), By Application: (General Radiography, Orthopedic, Oncology, Dentistry, Cardiovascular), By End-User: (Hospitals, Diagnostic Centers, Specialty Clinics) across global and regional markets. Further, analysis and outlook across 21 countries in North America, Europe, Asia Pacific, Middle East, Africa, and South America are provided in the study.

Computed Radiography and Digital Radiography Industry Overview

Compact Imaging Systems Enhancing Clinical Workflow Efficiency

The Computed Radiography (CR) and Digital Radiography (DR) industry continues to advance through innovations focused on workflow optimization, imaging quality, and patient safety. Recent systems showcased at the Radiological Society of North America (RSNA) exhibition were specifically engineered with compact mechanical footprints to accommodate healthcare facilities with limited imaging room space. These configurations combine advanced automated tracking technologies with high-resolution wireless flat-panel detectors, enabling more efficient patient imaging procedures. By reducing the need for extensive manual patient positioning, the systems help radiologic technologists streamline examination workflows while maintaining consistent imaging performance. Additionally, the integration of advanced detector technology contributes to minimizing radiation exposure thresholds, supporting the industry's continued emphasis on dose optimization and patient safety.

Automation Technologies Improving Imaging Accuracy and Productivity

Automation is becoming a defining feature of next-generation radiography systems as healthcare providers seek to enhance operational efficiency and imaging consistency. Recent system upgrades incorporate automated positioning assistance, optical-sensor-driven patient alignment, and real-time radiation dose tracking optimization. These features utilize intelligent mechanical synchronization between the X-ray tube, wall stand, and table bucky to automate positioning processes that traditionally required significant manual adjustment. By reducing workflow friction and minimizing operator variability, automated radiography platforms help ensure reproducible image quality across a wide range of clinical examinations. The combination of automated mechanics and intelligent imaging controls supports greater productivity for radiologic technologists while contributing to improved patient throughput and examination standardization.

Strategic Corporate Restructuring Supporting Technology Investments

The CR and DR industry is also being influenced by strategic organizational restructuring initiatives designed to accelerate product development and strengthen regional market responsiveness. Recent corporate separation strategies have established independent business structures optimized to manage localized supply chains and targeted innovation programs. These newly formed organizations are positioned to pursue region-specific capital investments focused on both computed radiography retrofit solutions and native digital radiography detector technologies. The separation enables each company to allocate resources toward the unique needs of its respective clinical markets while supporting faster product development cycles and more agile operational decision-making. As healthcare providers continue transitioning from legacy CR systems to advanced DR platforms, such strategic restructuring efforts are expected to facilitate greater investment in detector technologies, workflow-enhancing imaging solutions, and localized customer support capabilities.

Computed Radiography and Digital Radiography Market Trends, Growth Drivers, Competitive Landscape, and Future Opportunities

The global Computed Radiography and Digital Radiography market is witnessing increasing investments in innovation, product development, digital transformation, artificial intelligence integration, healthcare infrastructure expansion, and strategic partnerships across developed and emerging economies. Key Companies in the industry include- Siemens Healthineers AG, GE HealthCare Technologies Inc., Koninklijke Philips N.V., FUJIFILM Holdings Corporation, Canon Medical Systems Corporation (Canon Inc.), Carestream Health, Inc., Agfa-Gevaert Group, Konica Minolta, Inc., Shimadzu Corporation, Shanghai United Imaging Healthcare Co., Ltd.. The Computed Radiography and Digital Radiography market is expected to remain one of the most closely watched segments in the global healthcare industry, with companies focusing on niche market segments. As healthcare systems across the US, Europe, Asia-Pacific, Latin America, and Middle East & Africa continue to prioritize efficiency, access, and innovation, the Computed Radiography and Digital Radiography industry outlook remains shaped by rising healthcare expenditure, demographic change, digital transformation, and product innovation.

The report provides detailed market analysis including-

-

Growth Computed Radiography and Digital Radiography Market size outlook across 3 scenarios- High growth, reference, and Low growth cases

-

Market Trends, Drivers, Potential Opportunities, and Challenges faced by Computed Radiography and Digital Radiography companies

-

Porter’s Five forces analysis- Bargaining power of buyers and sellers, Threat of Substitutes and new entrants, and Intensity of competitive rivalry

-

Detailed SWOT Analysis of global and regional Computed Radiography and Digital Radiography markets

-

Competitive analysis including business description, product analysis, and financial profiles

-

Key country specific analysis detailing key factors shaping the short-term and long-term outlook

-

Recent industry developments and news including mergers, acquisitions, product launches, expansions, and company announcements

Computed Radiography and Digital Radiography Market Competitive Benchmarking and Company Analysis

Leading companies in Computed Radiography and Digital Radiography industry include- Siemens Healthineers AG, GE HealthCare Technologies Inc., Koninklijke Philips N.V., FUJIFILM Holdings Corporation, Canon Medical Systems Corporation (Canon Inc.), Carestream Health, Inc., Agfa-Gevaert Group, Konica Minolta, Inc., Shimadzu Corporation, Shanghai United Imaging Healthcare Co., Ltd.. The Computed Radiography and Digital Radiography market remains moderately to highly fragmented, with competition expected to intensify as companies accelerate investments in innovation, geographic expansion, strategic partnerships, and portfolio diversification through 2034. In developed markets such as the United States, Germany, France, the United Kingdom, and Canada, competition is increasingly centered on innovation, reimbursement positioning, and value-based healthcare solutions. Meanwhile, emerging markets including China, India, Brazil, and countries across the Middle East and Africa continue to present significant opportunities for expansion due to rising healthcare expenditure, growing patient populations, and increasing access to healthcare services.

What to expect in US Computed Radiography and Digital Radiography Markets in 2026 and beyond- Market Size, Share, Growth Rate, and Forecast to 2034

The US healthcare expenditure is forecast to reach $8.2 Trillion in 2034 from $5.5 Trillion in 2026 based on the National Health Expenditure Accounts (NHEA) data. With an aging population, rising chronic disease burden, and increasing migration toward minimally invasive and outpatient care, the Computed Radiography and Digital Radiography market remains one of the strongest-performing segments in the country.

The US Computed Radiography and Digital Radiography Companies are opting new business models, optimized pricing models, industry partnerships, and AI-enabled back end transformations to enhance efficiency and cost management. The US Computed Radiography and Digital Radiography market faces successive waves of challenging trends, with strong opportunities across select segments. The CMS plan to implement Medicaid from 2027 is driving states to build eligibility verification systems throughout 2026. Looking ahead to 2034, we anticipate stronger results underpinned by opportunities exist across Computed Radiography and Digital Radiography industry. On the medical device front, over 7,000 device manufacturers continue to gain from increasing demand from demand for implantable devices, surgical instruments, monitoring equipment, and diagnostic systems.

Canada- Proximity to the US and healthcare similarities to EU5 countries fuel sales of Canadian Computed Radiography and Digital Radiography markets

Canada's strong Computed Radiography and Digital Radiography sales performance is underpinned by an aging population and a well-developed healthcare infrastructure. Steady growth in new brand spending in rural and urban locations fuel the long-term prospects of small and medium-sized enterprises across medical, diagnostic, and therapeutic devices. The Canadian Computed Radiography and Digital Radiography market presents significant opportunities for U.S. exporters of medical devices, with the U.S. being Canada’s largest trading partner for this sector. Potential advantages including specialized materials, advanced manufacturing techniques, and digital technologies support the launch of new products in the country.

Germany Computed Radiography and Digital Radiography Trends and Perspectives to 2034- Financial sustainability, hospital restructuring, demographic pressures, and digitization of care delivery continue to shape the German healthcare industry.

Germany continues to remain the largest Computed Radiography and Digital Radiography market in Europe, driven by over €600 Billion healthcare expenditure, €12 Billion medical device R&D expenditure, statutory health insurance system covering 90% German population, nationwide rollout of the electronic patient record (ePA), and large-volume of Computed Radiography and Digital Radiography population. In particular, Research and development in Germany fuels the commercialization of cutting-edge technologies. Companies across the Germany Computed Radiography and Digital Radiography industry value chain are focusing on both domestic markets and exports. The country is also driving digital adoption with the Hospital Future Act driving hospitals to upgrade their information systems by 2027. Over the forecast period, aging population, rising healthcare costs, and increasing procedural volumes drive the Computed Radiography and Digital Radiography market outlook.

France Market Size, Growth Rate, and Forecast Analysis to 2034- Universal healthcare system, high public healthcare expenditure, and strong government support Computed Radiography and Digital Radiography sales through 2034

France Computed Radiography and Digital Radiography companies are emphasizing on opportunities for rapid, at-scale innovation to boost profitability over the long-term. The country’s National Health Insurance spending target (ONDAM) estimates 3.7% growth in the country’s healthcare expenditure. Over the forecast period, expenditure control measures, chronic disease management initiatives, workforce reforms, and efforts to improve system efficiency drive the long-term prospects.

The biggest 2026 policy frame is the PLFSS 2026. The law sets the Maladie branch spending target at €271.4 billion for 2026 and fixes the ONDAM at €117.5 billion for city care, €112.8 billion for health establishments, and €18.3 billion for elderly-care establishments and services. France’s market is also being pulled by demographics. INSEE estimates that on 1 January 2026 France had 69.1 million inhabitants, with 22% aged 65 or over. INSEE also reported that 2025 births were 645,000 and deaths were 651,000, producing a negative natural balance of about 6,000 for the first time since the end of the Second World War.

UK Computed Radiography and Digital Radiography Market Size, Share, and Growth Projections to 2034- Rapid growth driven by new and existing brands across the industry value chain

Small high-need consumer segments remain key priority of Computed Radiography and Digital Radiography distributors in the UK industry. Continuous launch of new products coupled with high expenditures support the market outlook. The UK Government financing remains the dominant funding source at 81.3% of total healthcare expenditure, or £280 billion in 2025. According to the ONS, total healthcare spending grew 7.7% nominally and 3.9% in real terms from 2024 to 2025. Similarly, out-of-pocket spending was £49 billion (14.1%) and voluntary health insurance was £9.5 billion (2.8%). The market is driven by rapid digital adoption with NHS England’s plan to give more than 500,000 staff access to new AI tools.

China Computed Radiography and Digital Radiography Market Growth Drivers, Revenue Trends, and Forecast- Medical insurance coverage is rapidly expanding over the past few years

China Computed Radiography and Digital Radiography market is undergoing a structural shift from hospital-centric care toward a more integrated system emphasizing primary care, outpatient services, and long-term care. Chinese local players are emerging as a strong pillar of Computed Radiography and Digital Radiography industry, offering opportunities for both competition and partnership. Over the forecast period, new and innovative product launches remain key elements driving market outlook. China's healthcare industry is increasingly centered on expanding healthcare capacity, improving access to advanced treatments, and reducing dependence on imported technologies.

The National Healthcare Security Administration reported that by end-2024, China’s basic medical insurance covered 1.32662 billion people and the coverage rate was 95%. Regional disparities in consumer spending trends continue to become more pronounced in the Chinese Computed Radiography and Digital Radiography industry. Over the forecast period, demand will keep shifting toward geriatrics, chronic disease management, rehabilitation, long-term care, and outpatient care, while pricing pressure will remain intense in drugs and consumables because reimbursement.

India Computed Radiography and Digital Radiography Market Landscape: Current Size and Long-Term Growth Outlook - Increased pricing pressures in US market is encouraging domestic vendors to expand across India

Indian Computed Radiography and Digital Radiography market is witnessing the rapid emergence of an ecosystem that brings together diverse companies across the industry value chain. Further, large-scale healthcare public and private investments and a steady growth in chronic conditions is driving sales of pharmaceuticals and medical devices. Further, non-retail channel is experiencing volume decrease and patients are migrating to the retail. Indian medical device firms are also combining precision engineering with lower labor costs to make world-class diagnostics, robotics, and critical care devices.

Brazil Computed Radiography and Digital Radiography market remains price-driven, with products domestically manufactured and accessibility offering potential opportunities

Healthcare expenditure in Brazil exceeds 10% of GDP, with the country among the highest healthcare spenders in Latin America. ANS reported 53.2 million medical-plan beneficiaries in December 2025, while IBGE projects a steady rise in older-age cohorts, with people aged 60+ already representing about 23% of the population. The price sensitive market access is broad through the public system, private coverage adds a sizeable premium layer, and reimbursement, procurement, and hospital efficiency remain key buying drivers.

Middle East and Africa Computed Radiography and Digital Radiography Industry Trends and Perspectives to 2034

According to the World Bank, the Middle East and North Africa population exceeds 500 million, while Sub-Saharan Africa's population exceeds 1.2 billion, making the broader MEA region one of the fastest-growing healthcare demand centers globally. The GCC countries including Saudi Arabia, United Arab Emirates, Qatar, and Kuwait continue to account for a disproportionately large share of regional healthcare spending. Government-led programs such as Saudi Arabia's Vision 2030 are accelerating investments in hospital infrastructure, private-sector participation, medical technology adoption, and healthcare digitalization. On the other hand, South Africa, Egypt, Nigeria, and Kenya remain key healthcare markets due to their large populations, expanding private healthcare sectors, and growing investments in healthcare delivery systems.

Computed Radiography and Digital Radiography Market Segmentation

By Technology:

Computed Radiography

Direct Digital Radiography

By Portability:

Fixed Systems

Portable Systems

By Type:

Static Imaging

Dynamic Imaging

By Application:

General Radiography

Orthopedic

Oncology

Dentistry

Cardiovascular

By End-User:

Hospitals

Diagnostic Centers

Specialty Clinics

Top Companies in Computed Radiography and Digital Radiography Industry

Siemens Healthineers AG

GE HealthCare Technologies Inc.

Koninklijke Philips N.V.

FUJIFILM Holdings Corporation

Canon Medical Systems Corporation (Canon Inc.)

Carestream Health, Inc.

Agfa-Gevaert Group

Konica Minolta, Inc.

Shimadzu Corporation

Shanghai United Imaging Healthcare Co., Ltd.

Countries Included

-

North America- US, Canada, Mexico

-

Europe- Germany, France, UK, Spain, Italy, Nordics, Others

-

Asia Pacific- China, India, Japan, South Korea, Australia, Southeast Asia, Others

-

Latin America- Brazil, Argentina, Others

-

Middle East and Africa- Saudi Arabia, UAE, Other Middle East, South Africa, Other Africa

Latest Market Updates In Healthcare

Support this report with fresh, same-industry updates that strengthen topical depth and internal linking.

By Technology:

Computed Radiography

Direct Digital Radiography

By Portability:

Fixed Systems

Portable Systems

By Type:

Static Imaging

Dynamic Imaging

By Application:

General Radiography

Orthopedic

Oncology

Dentistry

Cardiovascular

By End-User:

Hospitals

Diagnostic Centers

Specialty Clinics